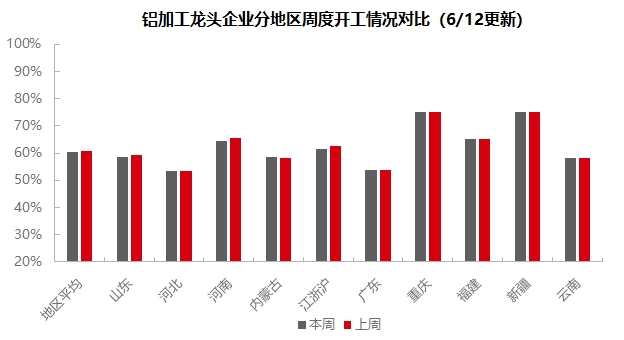

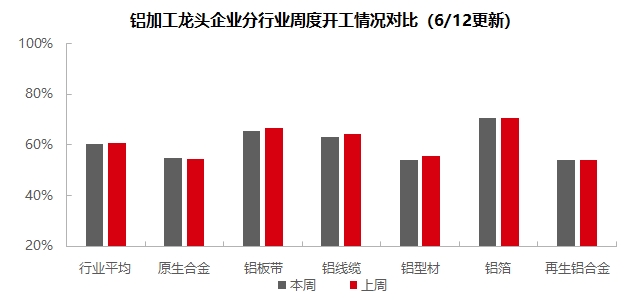

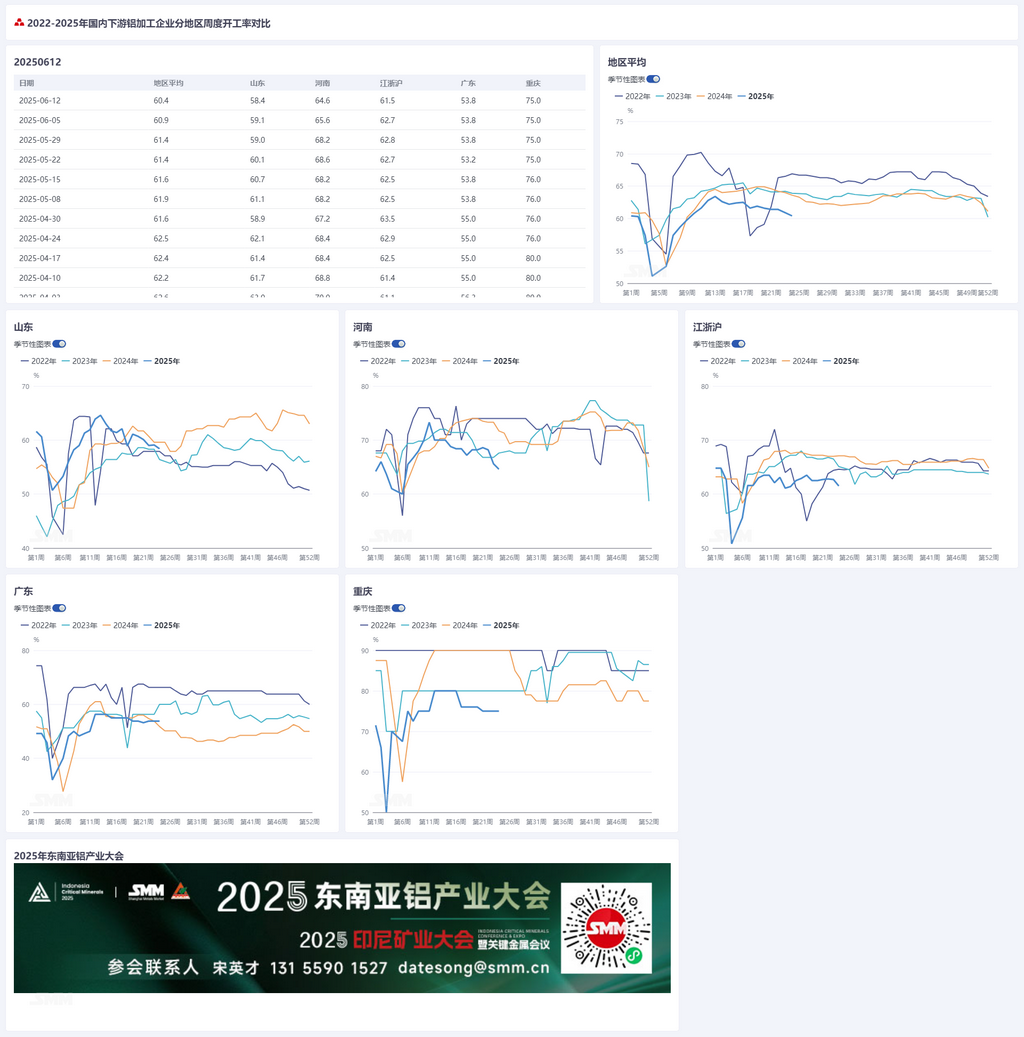

On June 5, 2025:

As June arrives, the downstream aluminum processing sector is deeply entrenched in the off-season atmosphere, with the weekly operating rate declining by 0.4 percentage points WoW to 60.9%. By segment, the operating rate in the primary aluminum alloy industry has remained relatively stable compared to May. Most enterprises in the industry reported moderate stability in their orders on hand, and there has been no pullback in production operating rates. In the aluminum plate/sheet and strip segment, aluminum prices remained high during the week, leading to strong wait-and-see sentiment among downstream customers. Additionally, as the market transitions between peak and off-peak periods, overall demand weakened, causing operating rates to decline in some sample enterprises. In the aluminum wire and cable segment, as the peak delivery period has passed, enterprise enthusiasm for procurement and production has waned, and market order performance has also weakened and become more fragmented. It is necessary to continuously monitor the arrival of the next delivery cycle and the order performance in market segments such as PV, wind power, automotive wiring harnesses, and infrastructure. This week, the operating rate in the aluminum extrusion segment showed divergence. New orders in various construction material fields were sluggish, leading to a decline in operating rates. Affected by the weak procurement sentiment of downstream component manufacturers, the operating rate of PV frame extrusion plants also declined. Despite the lukewarm performance of the NEV segment, relatively saturated orders in the 3C sector, power pipelines, and rail transit provided some support to operating rates. In the aluminum foil segment, the current industry processing fee has reached the cost floor. Under the pressure of total output assessment, enterprises are compelled to adopt a "volume discount" strategy. Meanwhile, the continuously rising finished product inventories in recent times have become another constraining factor suppressing processing fees. It is necessary to continuously monitor destocking conditions. In the secondary aluminum segment, although aluminum prices stabilized and rebounded during the week, downstream enterprises' procurement willingness remained tepid, and demand continued to slump, with both domestic market and export orders showing varying degrees of decline. SMM expects that the weekly operating rate of downstream aluminum processing may decline slightly by 0.1 percentage point MoM to 60.8% next week.

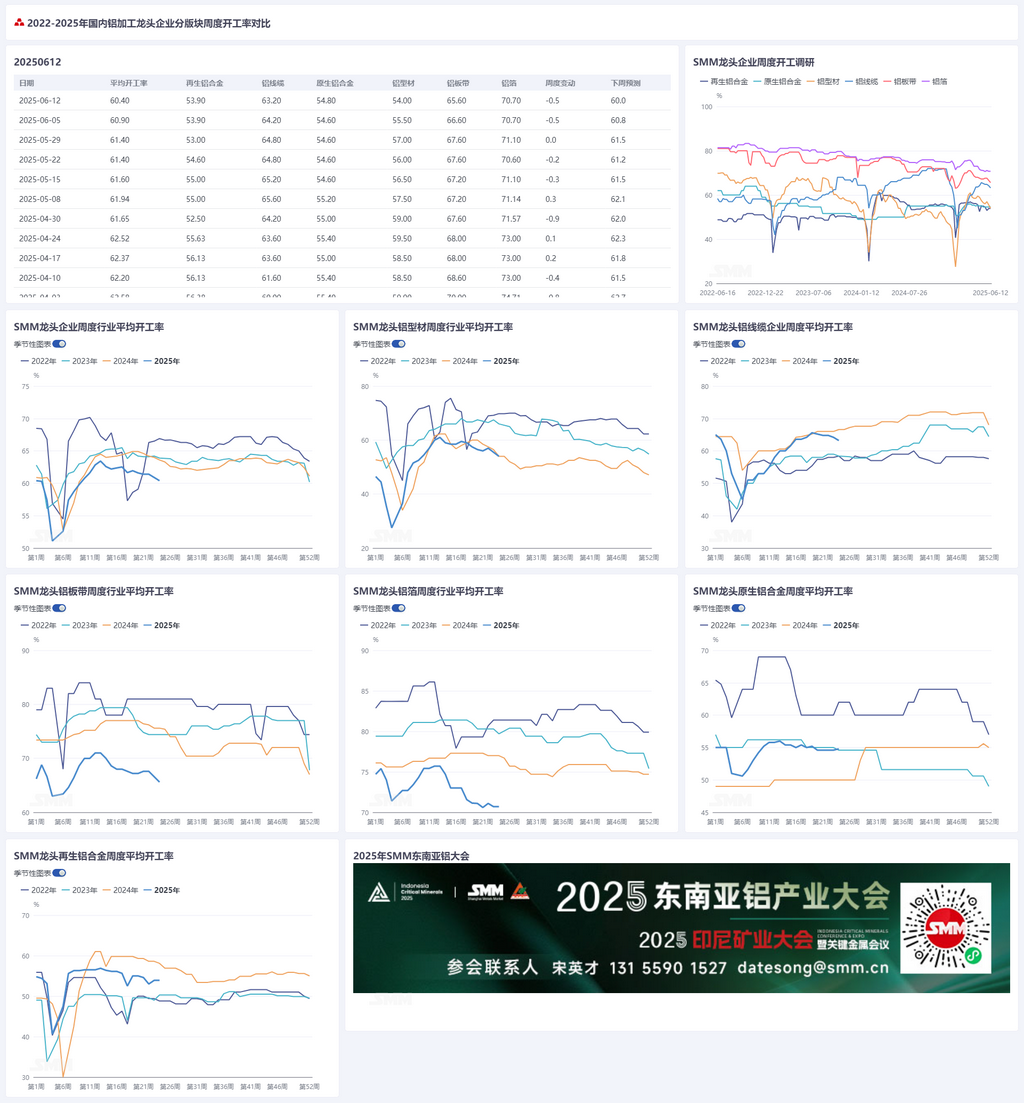

Primary Alloy: This week, the operating rate of leading enterprises in the primary aluminum alloy industry increased slightly by 0.2 percentage points from the first week of June to 54.8%. In the second week of June, the operating rate in the primary aluminum alloy industry remained largely unchanged compared to May. Currently, most enterprises have good order stability, and there has been no pullback in production operating rates. Given the relatively stable performance of both export data and domestic demand in the downstream aluminum alloy wheel hub segment, several primary alloy enterprises remain optimistic about subsequent operating performance. Whether to adjust production pace will depend on subsequent order conditions. Some enterprises also reported that, influenced by the expectation of reaching full production targets in H1 and the promotion of liquid aluminum alloying, they still have plans to increase production in June. Looking ahead, under the dual constraints of off-season factors and unclear tariff negotiations, coupled with the potential inhibition of consumption performance due to the continuous rise in short-term aluminum prices, which may transmit to the upstream raw material end, the operating rate in the primary aluminum alloy industry may continue to be in the doldrums. A substantive trend reversal awaits the implementation of Sino-US consultation details.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading enterprises in the aluminum plate/sheet and strip sector decreased by 1 percentage point WoW to 65.6%. Mid-week, aluminum prices continued to surge sharply, strengthening the wait-and-see sentiment among downstream customers, who slowed down the pace of cargo pick-up. Some sample enterprises, constrained by the high aluminum prices, temporarily slowed down their production pace. In terms of exports, positive news emerged from the Sino-US consultation meeting, easing the nerves of domestic aluminum plate/sheet and strip export enterprises. End-users such as home appliances, kitchen and bathroom products, and industrial equipment maintained normal export volumes. However, it was still difficult to offset the overall weak domestic consumption situation, and the operating rate of the entire industry continued to decline. As the off-season in June is about to reach its halfway point, it is predicted that the operating rate of aluminum plate/sheet and strip will continue to be in the doldrums in the subsequent period.

Aluminum Wire and Cable: This week, the operating rate of leading enterprises in the aluminum wire and cable sector stood at 63.2%, down 1% WoW. As we have entered mid-June, the industry has cooled down after experiencing a two-month concentrated delivery cycle. Leading enterprises indicated that, thanks to the implementation of the second batch of ultra-high voltage projects, they expected orders to be replenished, and the operating rate remained resilient. However, with the upward shift in the center of aluminum prices, the production enthusiasm of small and medium-sized enterprises has weakened significantly, with poor procurement efforts and a gradually spreading wait-and-see sentiment. In terms of orders, this week, the bid winners for the first joint procurement in the north-west China region in 2025, as well as the agreement inventories for low-voltage power cables and overhead insulated conductors, were announced. Meanwhile, orders for agreement inventories of overhead insulated conductors in central China and the Sichuan and Chongqing regions were also confirmed. Orders for overhead lines and power cables from wire and cable factories continued to grow. Combining the production schedules and order expectations of the factories, it is expected that the operating rate of wire and cable will remain in the doldrums in the short term. Close attention should be paid to whether the delivery window for ultra-high voltage and power transmission and transformation projects in August will provide strong support for the operating rates of downstream factories.

Aluminum Extrusion: This week, the national operating rate for extrusions increased slightly by 1.5 percentage points WoW to 54.5%. In the building materials segment, the overall operating rate declined compared to last week. According to the SMM survey, leading enterprises in central China and east China reported a decrease in operating rates due to a decline in orders. However, some enterprises in south China reported that building materials were mainly used as reserves and would not halt production due to short-term low expectations. Despite maintaining a low operating rate, they would continue production according to their annual production plans, with finished product inventories increasing slightly. This week, the operating rates of sample enterprises producing PV frames continued to diverge. With the definite production cuts by downstream module manufacturers, the operating rates of some PV frame extrusion enterprises in east China and Hebei continued to decline. However, according to SMM, some small and medium-sized PV frame extrusion enterprises in southwest China maintained a high operating rate, mainly because their coating production line capacity was basically in line with the procurement demand of leading module manufacturers, and their operations remained at full capacity. Some automotive extrusion enterprises in east China reported that the growth in new orders remained sluggish. Although their operating rates remained stable this week, they reported that the production of orders on hand was gradually coming to an end. These enterprises were actively negotiating with customers for new orders to ensure production continuity. Some enterprises in South China reported that they remain optimistic about industrial materials and are confident about securing a significant number of new orders in H2. Regarding other industrial materials, some enterprises in east China reported that their deep-processing production lines are operating at a high rate. Enterprises reported the need to increase the proportion of high value-added products to maintain healthy cash flow, with their extrusion production lines basically operating at around 60%. SMM will continue to monitor the actual progress of order fulfillment in various sectors.

Aluminum foil: The operating rate of leading aluminum foil enterprises was recorded at 70.7% this week. The aluminum foil market remained relatively stable compared to last week. By product, demand for household foil, lunch box foil, and other products continued to decline, with processing fees remaining at a low level with no signs of recovery, and the crisis of finished product inventories loomed large. Battery foil and brazing foil production schedules remained normal, providing support for the industry's operating rate. It is expected that the operating rate of aluminum foil enterprises will fluctuate downward in the subsequent period.

Secondary aluminum alloy: The operating rate of leading secondary aluminum enterprises remained flat MoM, stabilizing at 53.9%. From the perspective of the week, the sample leading enterprises maintained a normal production rhythm, but the overall industry operating rate still faces downward pressure in the short term, mainly due to two factors: First, the demand side remains persistently weak, with downstream enterprises showing significantly low purchase willingness and a sluggish market trading atmosphere. Second, the cost pressure of raw materials has surged, with aluminum scrap prices closely following the rise in aluminum prices, driving up the production costs of secondary aluminum alloy. Currently, the theoretical loss margin in the industry continues to widen, further exacerbating cost-side pressure, prompting some enterprises to choose production cuts and adopt a wait-and-see attitude to cope with market uncertainties. The operating rate of leading secondary aluminum enterprises is expected to remain stable in the short term.

》Click to view SMM Aluminum Industry Chain Database

(SMM Aluminum Team)